Observer Effect

There’s a concept in physics called the observer effect. The act of observing a phenomenon changes the nature of that particular phenomenon. Over the past few weeks, I’ve thought about this idea and its relevance in the economic world. It factors into a well-documented theory on a passive investing bubble in public markets, but the effect also holds for the venture market as the downside of growth at all costs has shown its head.

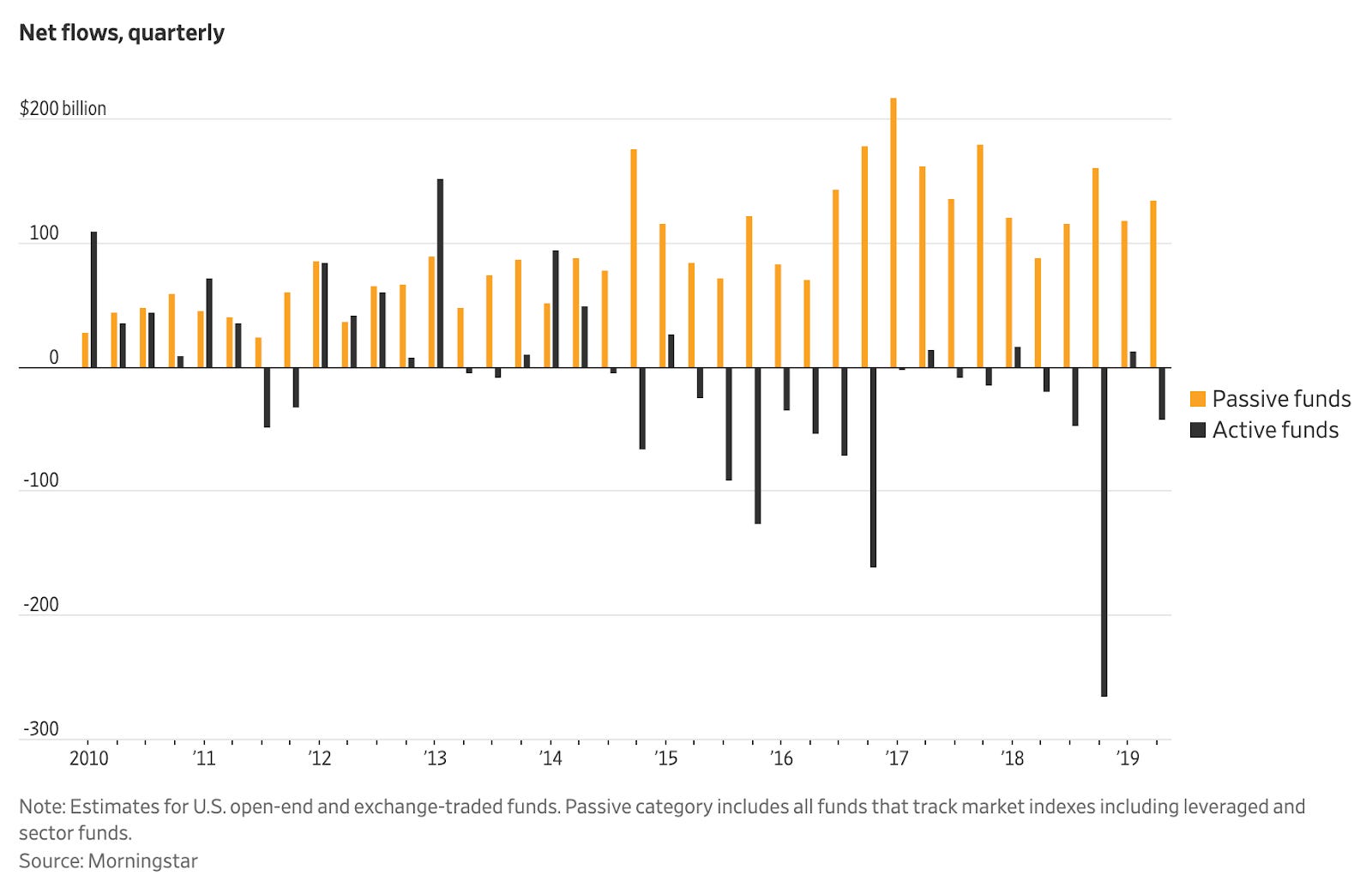

First, it’s important to set some context on market dislocation in public markets and the growth of passive assets. Trillions of dollars have flowed into passive funds, which buy and hold select indices of securities. Investors and individuals see the growth of the S&P 500, spearheaded by ultra-cap tech stocks, and pour money into low-cost funds that buy the index. The fatal flaw, according to critics, is that incoming dollars go towards purchasing securities in the index, and the volume of these purchases from Vanguard, Blackrock, etc. have an effect on the underlying securities that are distinct from the true “fundamental” value of the security.

https://www.wsj.com/articles/the-rise-of-passive-investing-marches-on-11563442202

Thus, people observe that the major indexes always go up, and feed the machine. The chained effect causes significant market dislocation, as the price continues to abstract away from the fundamentals in the basket. People bought into the indexes benefit from the emergent behavior, but security-level active managers feel the brunt.

How does the observer effect, playing out in the macro environment, map to the private technology investing sphere?

Peter Thiel (and others like Marc Andreessen) famously quipped that only a handful of tech startups matter every year, and the only thing that matters is finding and investing in these businesses. This observation is true. And to flesh it out a bit more, if only a few startups matter every year, and due to the size of global markets, marginal cost of information, and the power of increasing returns, these companies skyrocket in value - they escape the forces of mean reversion, meaning it doesn’t matter what price you pay in the early stages for them.

Here’s the rub -- once you make that observation, capital floods into the market and distorts it, changing the inherent nature of some of these businesses. SoftBank’s infusions are iconic examples. Similar to public markets, a select group will still continue to capture value (in this case, probably the top-tier platform venture funds), but many growth investors feel pain on a few fronts if the market turns. The road to recap is not a fun one.

When the music is playing and good times are rolling, the cracks in the edifice don’t expose themselves. Yet, during downturns, this market behavior proves harmful.

Hindsight is 20/20, but many startups took unnecessary capital injections and had aggressive burn rates without a sense of unit economics and the cost of growth. The justification was along the lines of, “well look at Amazon!” Amazon is a capital-intensive business that’s always aggressively grown out of necessity to capture and dominate the markets it finds itself in. But it’s worth noting that the franchise has always focused on free cash flow internally and ROIC. People pick and choose the lessons they want to take to heart.

If funding dries up for unicorns or other growth companies over $250M in valuation, you’re left with properties too expensive to be bought, which don’t lend themselves well to major restructuring due to light balance sheets. Intangible assets, a lightning rod for growth, quickly become a liability. There was a moment where Seth Klarman was thinking about engaging, but as one of the strictest disciplines of Graham’s net net philosophy, he’s found value elsewhere right now.

On the investing side, there was major career risk if you didn’t play in the game. If one is trying to return multiples on billions in assets, you need to put millions to work in the “screamers” (the companies that Thiel and Andreessen allude to), even if the company is at risk of over-capitalization. If you sit on the sidelines, you have partners and LPs to answer to. When the market begins to move the other way, reputation risk flips and comes from finding how to manage portfolios that have been built up.

This outlook may seem dire, but it’s meant to be more of an open exploration of the other side of the coin -- what are potential consequences of successful investing strategies that have driven returns over the past few years? We don’t pay enough attention to Wall Street and macro conditions as we feign isolation in the early-stage venture environment, but some of the same rules still apply. Spurning the efficient market hypothesis, constructed narratives and observations take their toll on market structures. These are not just markets of securities, they’re also markets of information and information front-running.

With contribution and feedback from Mutable Matter.